Tag:

Quantitative Investing

Specifying and Managing Tail Risk in Multi-Asset Portfolios (a summary)

Read More

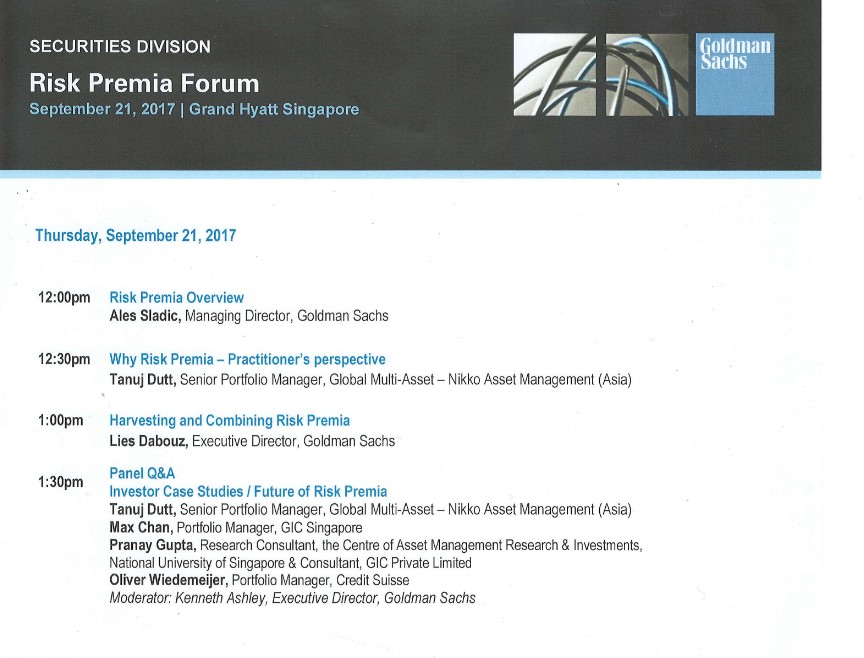

Risk Premia Forum – SINGAPORE

Read More

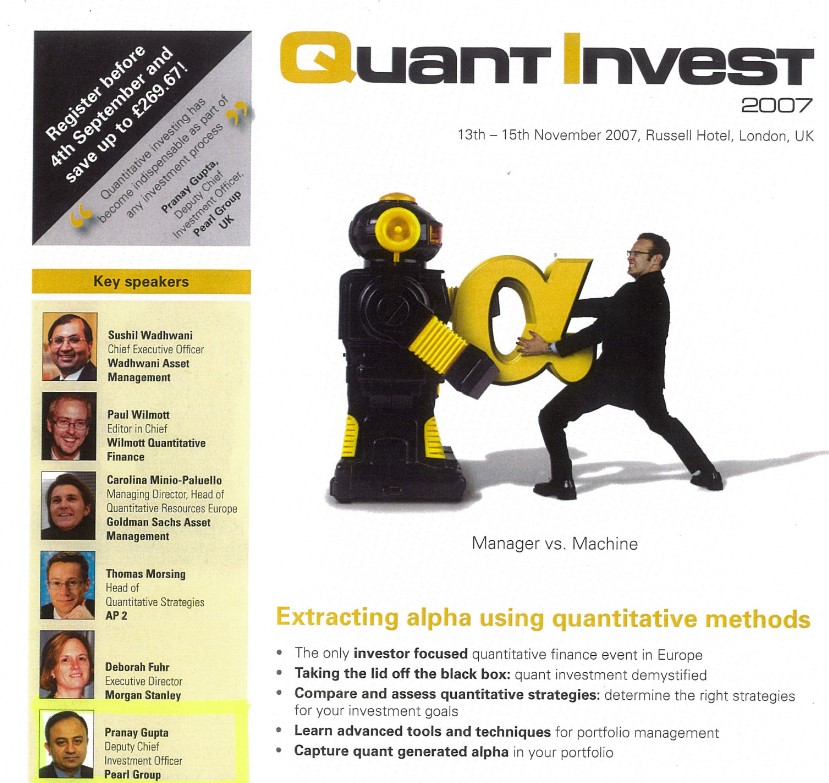

Quant Invest 2007 – LONDON, U.K.

Read More

Asia Risk Congress 2017 – SINGAPORE

Read More

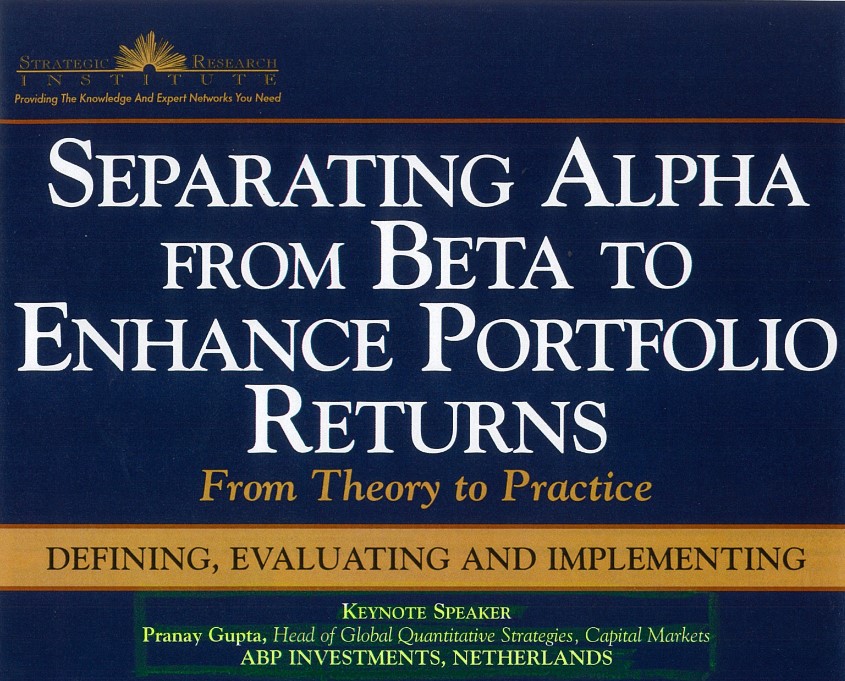

Separating Alpha From Beta To Enhance Portfolio Returns – PRINCETON, USA

Read More

Transaction Cost & Institutional Tradding 2003 – BARCELONA, SPAIN

Read More

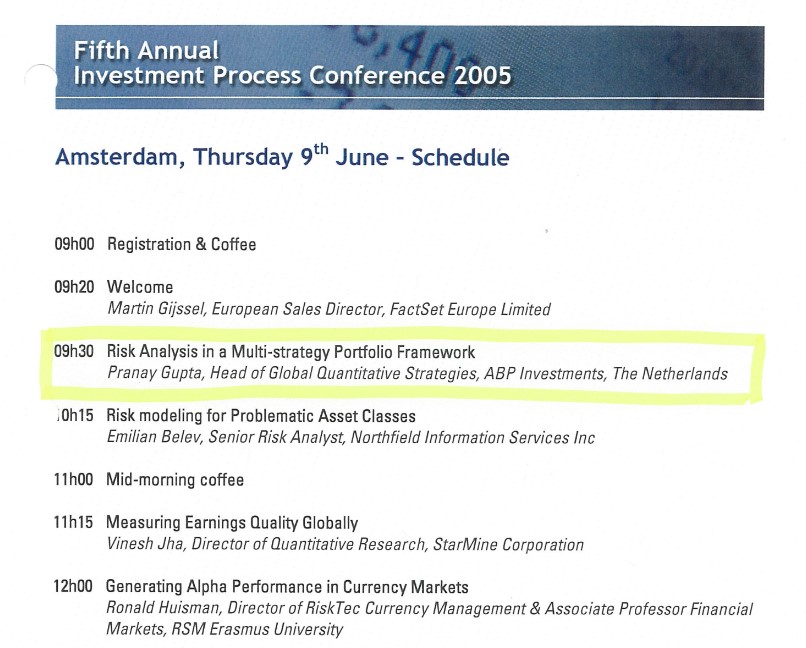

Fifth Annual Investment Process Conference – NETHERLANDS

Read More

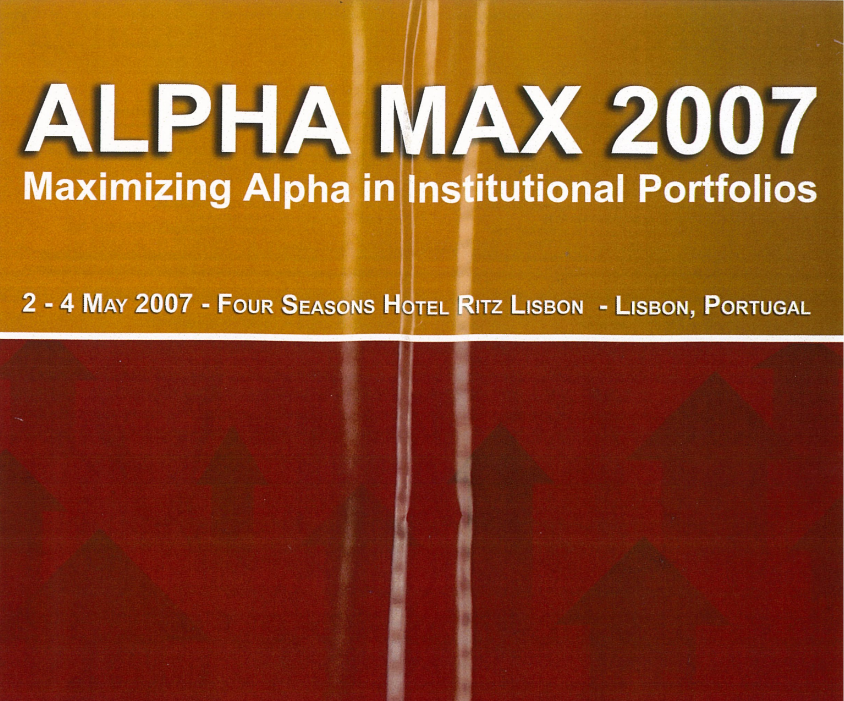

Alpha Max 2007 – LISBON, PORTUGAL

Read More

Alpha Isn’t Dead, but CAPM should be Killed

Read More